A new report released by PwC titled The Dawn of Electrified Trucking, Truck Study 2022: Routes to decarbonizing commercial vehicles gives an in-depth review of the industry and seeks to identify trends, trajectories and data, while offering reccomendations for the successful electrification of trucks. The report focuses in on three main themes: the predicited surge in electric vehicles; the urgent need for infastructure and the importance of total cost of ownership (TCO) to the decarbonisation journey.

PwC has forecast the breakthrough of electric trucks from 2030. According to the report, battery electric and fuel cell trucks are expected to account for 30% of the overall truck market by 2030 in the main global areas (North America, the EU and Greater China), followed by industry dominance from 2035 with 80% of overall sales being Battery Electric or Fuel Cell.

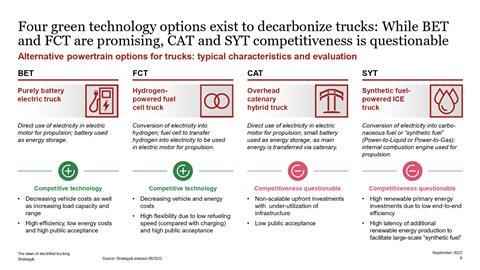

Battery electric and Fuel Cell are the most promising powertrain technologies for the future

The study notes how Battery Electric Trucks (BET) and Fuel Cell Trucks (FCT) are heavily regarded as competitive technologies for the future due to decreasing vehicle costs, declining energy prices and public acceptance. The success of BET and FCT is expected to grow, making them, currently, the most viable option in the electrification of commercial vehicles. In contrast, the report is less complimentary about the future for other alternative power solutions, such as overhead catenary hybrid trucks (CAT) and synthetic fuel-powered ICE trucks (SYT). Catenary trucks suffer from low public acceptance, non-scalable upfront investments and under-utilisation of infrastructure, while synthetic fuels are hampered by the cost of large scale production.

Although the cost gap shrinks over time - the study preficts medium-duty battery vehicles will be near cost parity with current ICEs by 2035 - the authors note that, simply, alternative powertrains translate into additional vehicle costs

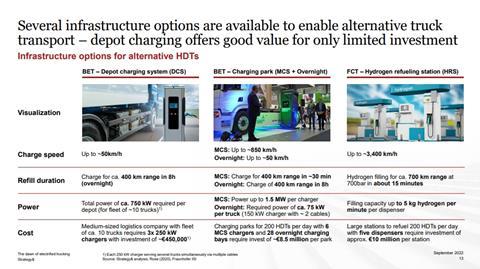

Infastructure requires urgent call for action

Turning to infrastructure, the decarbonisation of the sector requires serious efforts to build up public truck charging infrastructure. It is thought that investments of up to €1 billion are required to set up 120 Megawatt charging systems (MCS) by 2025. The report reconfirms three infastrucure options are required: depot charging system (DCS) for BET trucks, public charging for battery vehicles (Megqatt Charging Station + Overnight) and hydrogen refueling station (HRS) for Fuel Cell trucks.

Looking at long term goals, the report noted that in order to account for the growing demand, investment of up to €15bn for the Megwatt Charging Station network and €21bn for the Hydrogen Refueling Station network would be required by 2035.

PwC envision highway charging parks for Heavy Duty Trucks containing approximately 6 Megawatt Charging Station chargers and 28 overnight chargers for 34 truck bays. The development of a such a park alone would cost €8.5m.

However, the investment in the supply infrastructure is only a small share compared with the cost to produce the extra electricity required, the report notes.

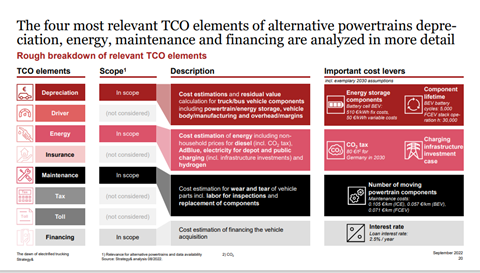

Total Cost of Ownership is the main driver for electrification

BET is expected to outperform Internal Combustion Engines (ICE) by 2025 onwards on total cost of ownership, say the authors, and by 2030 battery vehicles are expected to be 30% cheaper to run than diesel trucks.

Electric truck production will breakthrough in 2030 with more than 30% being zero emission vehicles.

The battery demand through the truck industry will surpass 800GWh in 2035. Currently, China and Europe are the front runners in this race.

The study noted that in 2030, a total of 900,000 battery and fuel cell trucks will be produced across North America, European and Chinese Markets. Approxamately 200,000 units in North America & Europe while China leads the charge with 500,000.

In its concluding pages the report offers four recommendations:

- Vehicle OEMS should build up an attractive zero-emission portfolio, with the focus on product cost and efficiencies

- OEMs should support infrastructure availability - something we have already seen with the CV Charging Europe joint venture with Traton, Daimler and Volvo

- Suppliers should prepare the value chain

- OEMs should offer attractive financing - we are already seeing this with popularility of pay-per-use or truck-as-a-service initiative

Download your copy of the report

–

Get involved in the decarbonisation conversation and comment below. We are keen to hear your thoughts and feedback

No comments yet